In March 2015, when George Osborne outlined the new concept of “making tax easier”, he said it would herald the death of the tax return. All the tax information relevant to an individual would be gathered into the taxpayer’s digital tax account, and the annual paper tax return would be consigned to history.

This was sold as a reduction in the administrative burden for taxpayers, but by the end of 2015 we were told that Making Tax Digital (no longer easier) would involve sending HMRC four updates per year. So the tax

return is not disappearing, it is merely changing its name and there will be four tax submissions (returns) a year rather than one.

This reminded of the time in the late 1990s when self-assessment was introduced. At the time I had a weekly slot on BBC Radio Merseyside reporting business news. On the morning self-assessment was announced the programme host introduced me by saying “Well the

government has made tax simpler and we’re all going to be filing our own tax returns – won’t that put accountants out of business?”

To which my reply was “No, we love it when the government simplifies things, it creates a lot more work for accountants.”

Well a close reading of the Finance Bill 2017

reveals that they’ve done it again, because Making Tax Digital for Business (MTDfB) will involve at least six additional tax submissions (note, not returns) per year, not four.

You couldn’t make it up!

Quarterly updates

The requirement to make periodic updates to HMRC says: “The regulations may not require financial information about the business to be provided more often than once every 3 months.”

Those regulations have not been published yet, but HMRC has made it clear that the maximum period an update can cover is three months. Although a taxpayer

may submit more frequently updates if they wish, anything more than quarterly updates will not be required.

It is worth noting that a set of quarterly updates will be required for each trade or business undertaken by the taxpayer. Thus, a self-employed individual who also has some rental income will have to submit a set of quarterly updates for their self-employed trade, and another set of

quarterly updates for their lettings business.

End of period statement

The updates are not required to include any accounting adjustments, as those adjustments are to be included (if necessary) in an “end of period statement”. This is the fifth submission to

HMRC.

This end of period statement (EoPS) is the point at which the taxpayer declares they have submitted complete and correct information regarding their trade. HMRC has said this will be set at the earlier time of 10 months after the accounting period end or the next 31 January.

Note that a

separate EoPS will be required for each trade or business undertaken by the taxpayer.

Final declaration

In addition to submitting the end of period statement the taxpayer will be required to make a “final declaration”. This is the new name for the annual tax return. The final declaration is needed

to report any income which has not been reported to HMRC through an EoPS, such as savings or employment income, and to make any necessary claims. The deadline for submitting the final declaration is on or before 31 January in the year after the end of the tax year, or if later, the last day of the period of three months beginning with the date of a notice issued by HMRC.

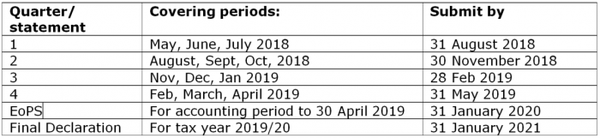

Example

Dave has a sole-trade business with a year end of 30 April, which has a turnover of £90,000 per year. He will start making quarterly reports under MTDfB from the accounting period that begins 1 May 2018. His quarterly updates must be submitted within one month of the end of each three-month period that starts on 1 May, and the other

declarations and statements must be submitted as follows: