Hi

The UK government will require electronic invoicing of all VAT invoices for business-to-business and business-to-government transactions from 2029 and has used its 2025 Budget to announce

its long-anticipated arrival .

In a short update in the Budget report, the government stated that to “drive productivity further”, it will require the use of e-invoicing for all VAT invoices for business-to-business and business-to-government transactions from 1 April 2029.

Responding to a

consultation launched in February 2025, the government today said it would be conducting “extensive stakeholder engagement from January 2026 to ensure stakeholder views and concerns are considered throughout the policy development process”.

It is expected that a final decision on the

exact details of the system will be published at the 2026 Budget.

What is e-invoicing?

E-invoicing is the direct digital exchange of invoice data between buyers’ and suppliers’ systems in a standard format. It is not simply emailing a PDF, Word doc or image to another person or

business.

Similar to the government’s Making Tax Digital (MTD) programme, software is required to send e-invoices. While specialist e-invoicing point solutions are available, accounting packages such as Xero have established capabilities in anticipation of a potential move.

Approaches to

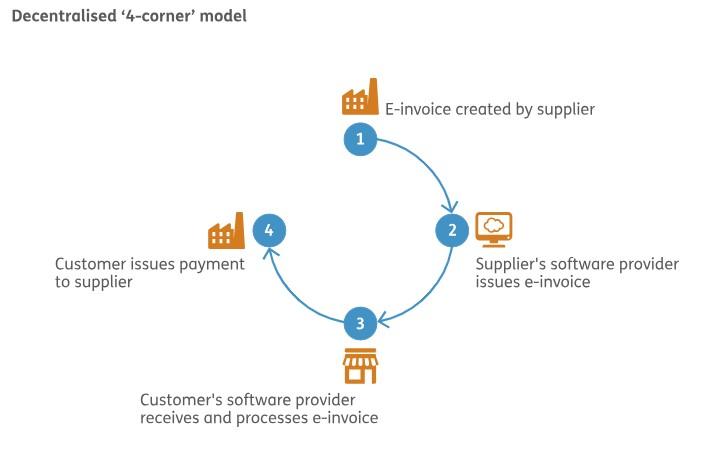

e-invoicing models and mandation differ around the world. We understand that the UK government currently favours a decentralised system, sometimes known as a four-corner model, as used in Australia and due to be implemented in Belgium in a matter of weeks.

In a four-corner system (see diagram below), the e-invoice is created by the supplier, the supplier’s software provider issues the

e-invoice, the customer’s software provider receives and processes the e-invoice, and the customer issues payment to the supplier.

The UK government has also set up a taskforce to develop a UK version of the PEPPOL (Pan-European Public Procurement On-Line) standard – a network used globally by most EU member states, plus Australia, Japan and Singapore.

E-invoicing pros and

cons

Proponents of e-invoicing point to its ability to process invoices faster and with fewer errors, cut out invoice duplication, avoid fraudulent activity such as criminals intercepting invoices and changing bank details, and allow for a more streamlined audit and reporting process.

Widespread adoption of e-invoicing in the UK could also provide HMRC with more information it can use to close the gap between tax owed and tax collected. However, critics point to the additional administration and cost burdens placed on businesses forced to purchase, learn and use external software to comply, particularly for smaller organisations or those that send or receive relatively few invoices.

Current state of e-invoicing

E-invoicing technology has been in use globally for more than 20 years, and around 130 countries have (or are in the process of) implementing e-invoicing structures and standards requiring businesses to use e-invoices for at least some transactions.

The format is already in place in many South and Latin American countries, and e-invoicing is a key part of the European Union’s VAT in the Digital Age (ViDA) reforms, currently due to roll out in 2030.

Until now, the UK has resisted adopting the format more widely following its exit from the European Union. With several years to plan and

prepare for e-invoicing UK businesses and their advisers will watch its rollout with interest.

Noel Guilford